NOTE: Bloomberg Second Measure launched a new and exclusive transaction dataset in July 2022. Our data continues to be broadly representative of U.S. consumers. As a result of this panel change, however, we recommend using only the latest posts in assessing metrics, and do not support referring to historical blog posts to infer period-over-period comparisons.

With alcohol delivery sales reaching new heights in the pandemic, American Airlines has recently announced its plans to start a wine delivery service to sell some of its surplus wine that isn’t being consumed on flights. However, an increasingly crowded category and rising consumer demand means that market share among DTC wine companies has shifted over time.

Our consumer transaction data shows which wine delivery companies gained and lost the most market share in the fourth quarter of 2020, and what is driving those shifts. More specifically, the data reveals market share gains and losses among specific customer segments as well as how spend is migrating between companies in the competitive set.

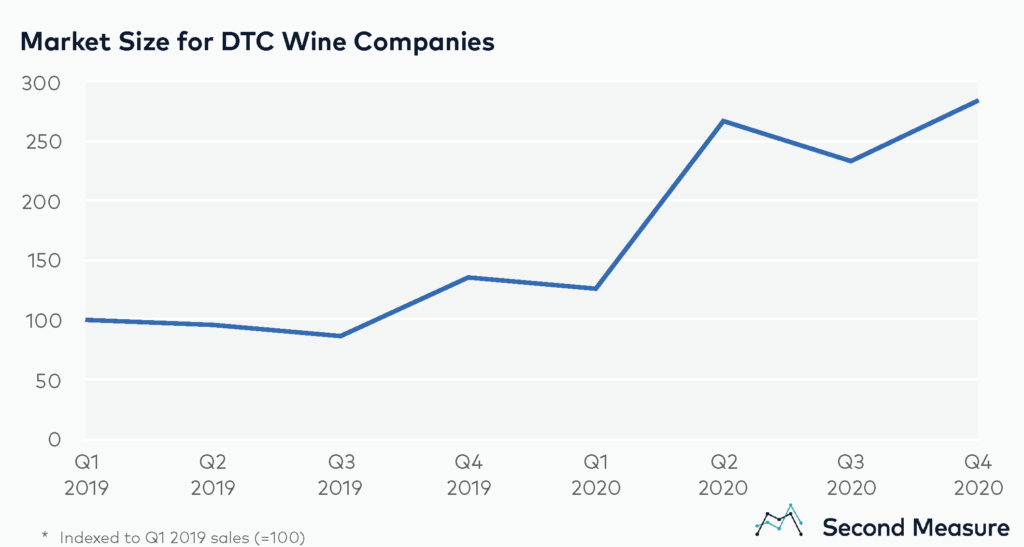

Market size more than doubled between Q1 and Q2 2020

Consumer spending trends reveal that the DTC wine market more than doubled between the first and second quarters of 2020, and has remained elevated. This market is composed of wine subscription clubs, ecommerce sites with a la carte purchases, and sellers with hybrid offerings.

Taking a closer look at the timeline, the Q2 2020 sales spike took place during the introduction of shelter-in-place orders, while a second spike in Q4 2020 coincided with the spike in wine sales during the holidays. Interestingly, as most brick-and-mortar establishments closed in the early months of COVID-19, some premium wineries that previously relied on restaurants or tasting rooms for sales also looked into expanding their sales channels to DTC wine companies.

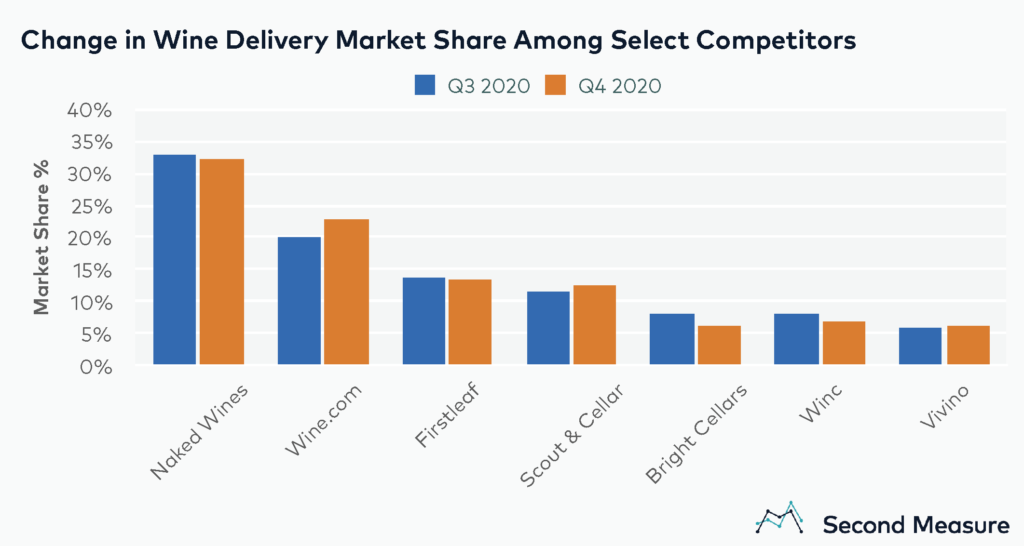

Wine.com gained the most market share points in Q4 2020

While wine delivery sales were up across the board, market share shifted from Q3 to Q4 of 2020 for some of the larger players in this competitive set. Notably, Wine.com gained about 3 percentage points in market share in Q4 2020. Market share also increased slightly for Vivino and Scout & Cellar.

Other wine delivery companies captured less market share in Q4 2020 than they did in Q3 2020. By percentage points, Bright Cellars lost the most market share between the third and fourth quarter of 2020, with a decrease of more than 2 percentage points. Naked Wines, Winc, and Firstleaf also experienced decreased market share quarter-over-quarter.

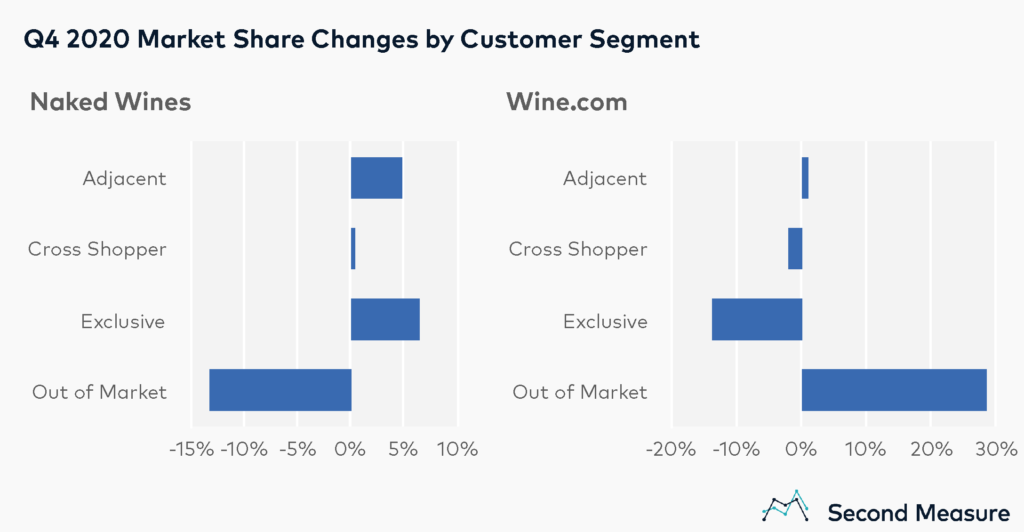

Both in-market spending shifts and new customers affected market share

Zooming in on the two largest companies in this competitive set, Naked Wines and Wine.com, we can see how spending shifts by customer type within a market. For example, Naked Wines’s market share gains were from consumers who were already in the DTC wine delivery market, while Wine.com’s gains were driven by new customers to the market.

Between Q3 and Q4 of 2020, the relative share growth—or growth rate of market share in dollars—was -2 percent for Naked Wines and 13 percent for Wine.com. Most of Naked Wines’ market share loss in Q4 2020 came from out of market consumers, defined as shoppers who had not purchased within the competitive set in the previous quarter. However, there was still some positive spend migration toward Naked Wines among in-market segments, especially adjacents (customers who shopped only at competitors in the previous quarter) and exclusives (customers who shopped only at Naked Wines the previous quarter). Interestingly, Naked Wines also has one of the highest customer retention rates among the competitive set, with 21 percent of customers making a repeat purchase four quarters after their initial purchase. Meanwhile, Wine.com’s Q4 2020 gains in market share were largely driven by out of market customers. Wine.com generally lost market share from in-market customers between the third and fourth quarters in 2020.

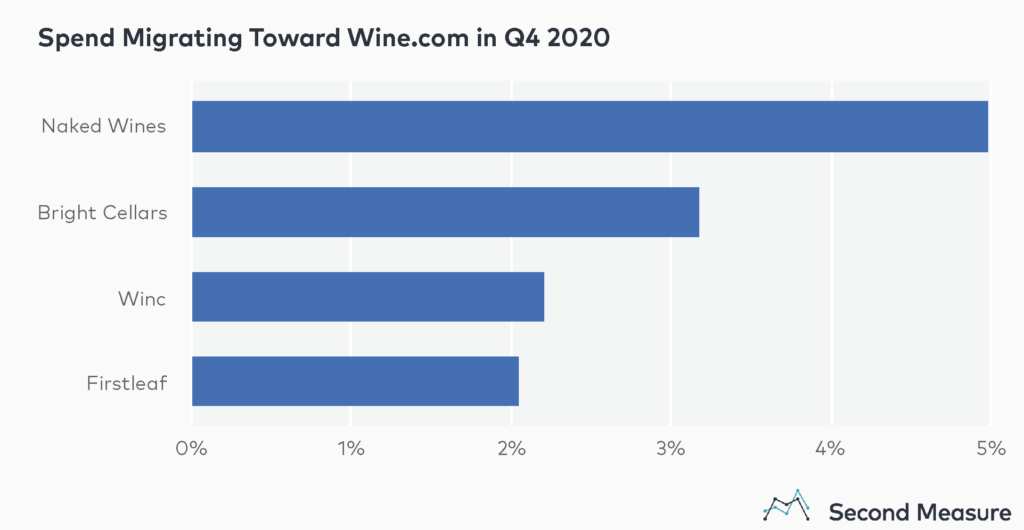

Spend migration data also indicates how much spend is lost to or gained from specific competitors. For example, an analysis of spend shift by competitor shows that of Wine.com’s 13 percent relative share growth between Q3 and Q4 of 2020, Naked Wines contributed 5 percentage points, more than any other company in the competitive set. Bright Cellars contributed 3 percentage points, followed by Winc and Firstleaf with roughly 2 percentage points.

Changing consumer tastes may impact future growth

In addition to more wineries and consumers embracing the online channel rather than strictly brick-and-mortar channels, there are other trends that may affect the future of the DTC wine industry. For example, millennials are not drinking as much wine as previous generations, favoring other beverages like hard seltzer. Furthermore, spending trends during the pandemic indicate that consumers are trying more premium wine bottles.

*Note: Second Measure regularly refreshes its panel and methods in order to provide the highest quality data that is broadly representative of U.S. consumers. As a result, we may restate historical data, including our blog content.