NOTE: Bloomberg Second Measure launched a new and exclusive transaction dataset in July 2022. Our data continues to be broadly representative of U.S. consumers. As a result of this panel change, however, we recommend using only the latest posts in assessing metrics, and do not support referring to historical blog posts to infer period-over-period comparisons.

Founded in 2012, Gymshark had been swimming along stealthily until it snapped up its first ever funding round from General Atlantic at a $1.3B valuation. Its focus has primarily been on building an influencer community and selling to consumers in its home country, the UK. Its founder, Ben Francis, is now looking to shift his direct focus to the U.S., and wants to establish the company’s U.S. presence in Denver, with shipment facilities in Ohio and California. Leading up to this planned expansion, Gymshark has been increasingly baiting new customers in the U.S.

New customer acquisition is driving sales growth

In Q2 2020, Gymshark’s new customer count was 1.73x compared to Q1 2018. Fabletics’ and SweatyBetty’s new customer counts increased 1.6x compared to Q1 2018, while LULU and Athelta’s new customer counts were relatively flat.

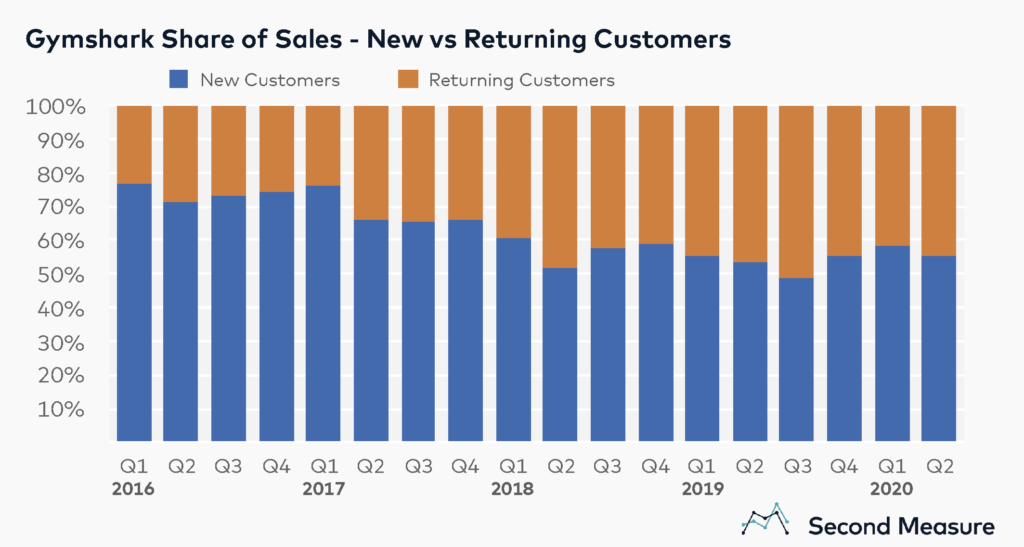

Although Gymshark has been growing, most of its revenue has historically come from new customer acquisition. However, over time, more of the company’s revenue is coming from returning customers.

In 2019, new customers contributed an average of 53 percent of Gymshark’s quarterly sales. This fell from 68 percent of sales in 2017, but is significantly higher than quarterly average share of sales from new customers for LULU and Athleta—17 percent and 20 percent, respectively. Similar to Gymshark, Sweaty Betty, another U.K.-based entrant, saw 56 percent of its sales come from new customers, on average, in 2019.

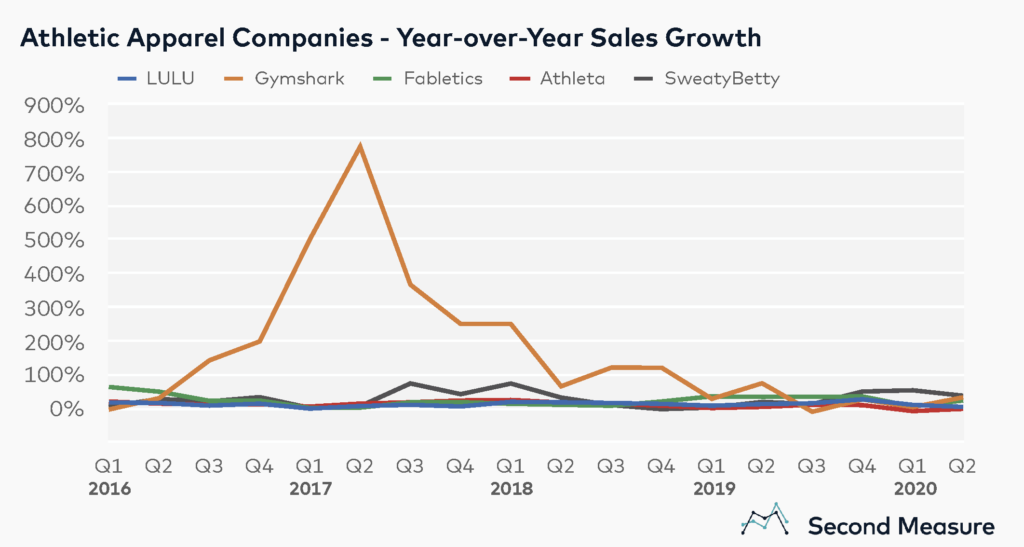

Gymshark’s sales growth is on par with leading athleisure brands

In 2019, LULU was the market leader with 56 percent share of sales. This was followed by Athleta at 27 percent share, Fabletics at 14 percent, Gymshark at 3 percent and SweatyBetty under 1 percent. However, Gymshark is quickly catching up to its peers in the U.S.

Gymshark’s sales grew rapidly in 2017. Gymshark saw its largest growth in Q2 2017, with sales growing 774 percent compared to Q2 2016. In recent quarters, Gymshark’s sales growth is in-line with that of Athleta, Fabletics, and LULU. Its Q1 2020 growth was impacted by the onset of the pandemic, with sales increasing only 4 percent. However, it bounced back in Q2 2020, with growth of 33 percent. Sweaty Betty proved to be the leader in terms of growth during COVID-19 with 54 percent growth in Q1 2020 and 38 percent in Q2 2020. Fabletics saw 24 percent growth in Q2 2020, whereas LULU only saw 4 percent growth and Athleta’s sales declined 1.4 percent compared to Q2 2019.

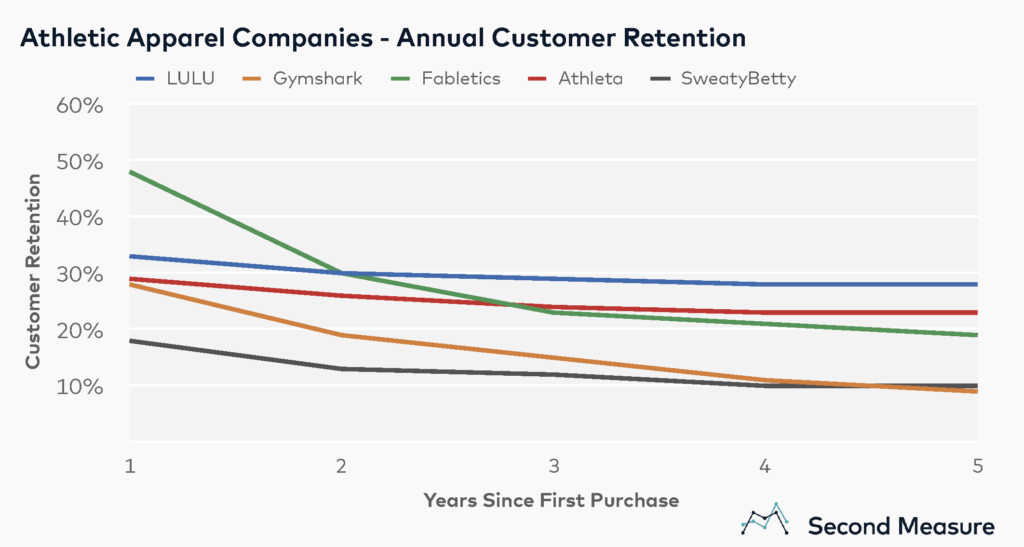

Gymshark’s retention trails that of its peers

Despite Gymshark’s strong new customer acquisition and on-par revenue growth, Gymshark has a lower annual customer retention rate than its competitors. Only 28 percent of Gymshark customers return a year after their first purchase, compared to 33 percent of LULU customers and 48 percent of Fabletics customers. It’s worth noting that Fabletics follows a subscription model, which helps its first-year retention.

Looking farther out, only 15 percent of Gymshark’s customers are retained after three years, which is roughly half of LULU’s 28 percent retention rate.