NOTE: Bloomberg Second Measure launched a new and exclusive transaction dataset in July 2022. Our data continues to be broadly representative of U.S. consumers. As a result of this panel change, however, we recommend using only the latest posts in assessing metrics, and do not support referring to historical blog posts to infer period-over-period comparisons.

As many Americans are returning to the office, pet owners are faced with the question of what to do with their pets while at work. That’s potentially good news for pet care companies, which struggled early in the pandemic as more people were staying home. In fact, the dog-walking platform Wag announced in February 2022 that it is planning its public debut via a SPAC deal. Its main rival, Rover (NASDAQ: ROVR), went public in August 2021, also through a SPAC merger. But pandemic recovery has differed for these two canine care companies. Consumer transaction data shows that Wag’s sales have not yet recovered to pre-pandemic levels, while Rover’s sales have skyrocketed over the past year. However, Wag’s average customer retention rates in 2021 were about twice as high as Rover’s.

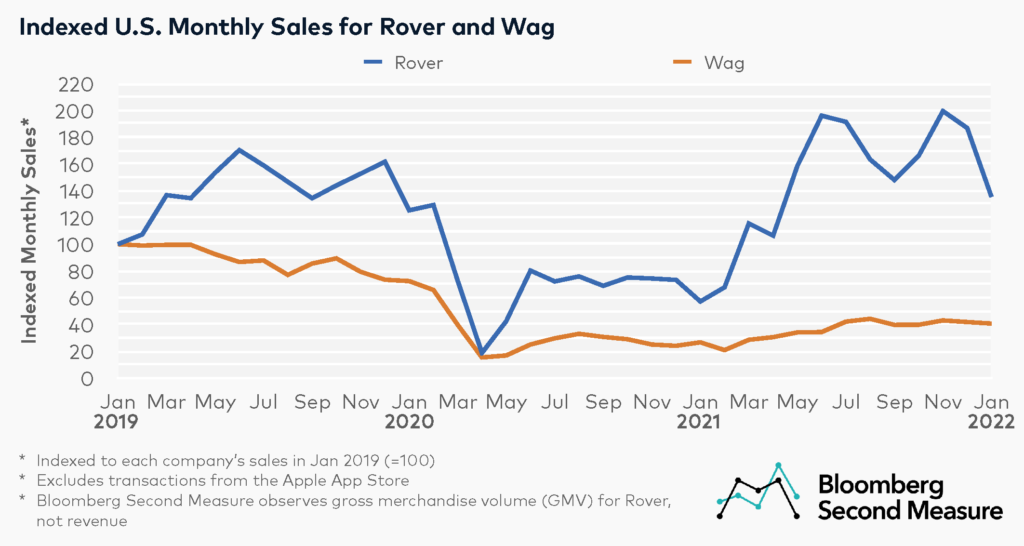

Rover’s sales growth outpaces Wag’s

Both Rover and Wag offer a variety of pet care services, including dog walking, home visits, pet sitting, and pet boarding. Rover also offers pet daycare and grooming, while Wag offers pet training. When it comes to sales, Rover remains the top dog. Rover’s U.S. monthly sales have exceeded pre-pandemic levels since May 2021. More specifically, Rover sales in January 2022 were up 8 percent compared to the same month in 2020, while Wag sales were down 44 percent. It is worth noting that Bloomberg Second Measure data excludes transactions through the Apple App Store, as well as as well as transactions from countries outside of the U.S.

In January 2022, Rover earned 91 percent of U.S. sales between the two companies, likely driven by a combination of higher customer counts and higher consumer spending compared to Wag. That month, Rover customers spent an average of $191 while Wag customers spent an average of $116. Notably, pet carers set their own rates on both services.

Rover has also expanded its reach in the pet care industry by acquiring competitors and partnering with large retailers. In 2017, Rover acquired the pet-sitting service DogVacay. In late 2020, Rover partnered with Walmart to offer its pet-sitting services through the retail giant’s new Walmart Pet Care program. As of February 2022, consumers are also able to book Rover’s pet care services through Petco.

Wag’s customers are more likely to stay

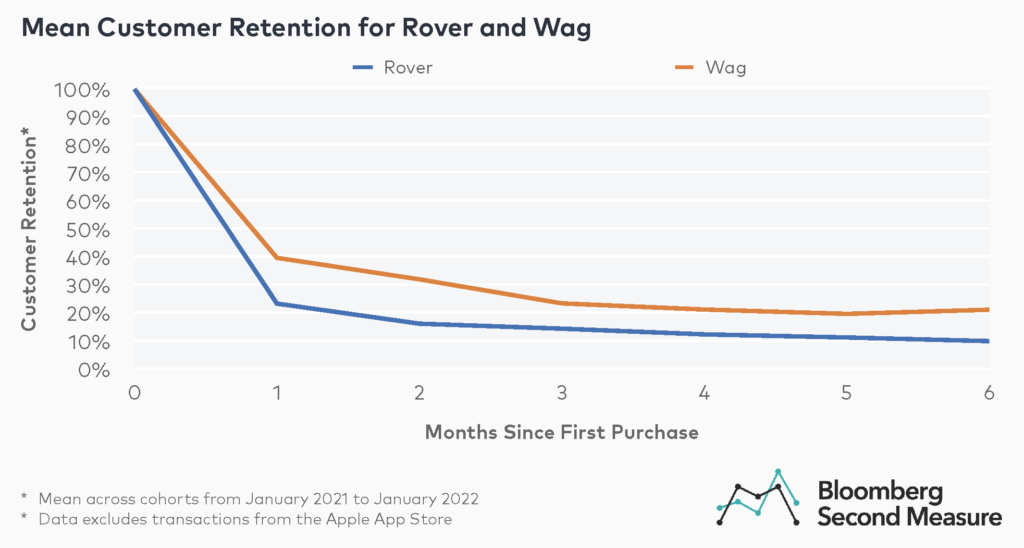

While Wag’s sales are down compared to pre-pandemic levels, its average customer retention in 2021 was higher than Rover’s. Among cohorts who signed up for Wag in 2021, an average of 21 percent made an additional purchase after 6 months. At Rover, only 10 percent were retained after 6 months.

Both companies see a significant dropoff in customers after the first month of purchase. On average, 40 percent of customers who signed up for Wag in 2021 made another purchase the following month, compared to 23 percent for Rover.

A likely reason for Rover’s lower customer retention is that three-quarters of its business reportedly comes from pet sitting or boarding, two services that may not be required as frequently as dog walking. Interestingly, Rover’s growth in bookings in summer 2021 closely followed trends related to increased air travel, suggesting an increase in consumers who were looking for a place to board their pets while they went on vacation.

Another factor that may impact retention rates is that Wag offers a premium subscription for $9.99 per month, which provides discounts on services booked through the app as well as waived booking fees. Rover does not currently offer a subscription program.

Wag is among the latest in a series of gig economy companies to prepare for a public debut. Delivery platforms Instacart and GoPuff are also expected to go public later this year.

*Note: Bloomberg Second Measure regularly refreshes its panel and methods in order to provide the highest quality data that is broadly representative of U.S. consumers. As a result, we may restate historical data, including our blog content.