NOTE: Bloomberg Second Measure launched a new and exclusive transaction dataset in July 2022. Our data continues to be broadly representative of U.S. consumers. As a result of this panel change, however, we recommend using only the latest posts in assessing metrics, and do not support referring to historical blog posts to infer period-over-period comparisons.

Any channel surfer who has quickly clicked past a TV shopping channel may be surprised to learn that QVC’s planned purchase of the Home Shopping Network (HSN) is about to turn these two televised shopping stations into North America’s third biggest online retailer, after Amazon and Walmart.

Those two giants may seem to be in an e-commerce league of their own, but our data reveals there is a customer base where QVC and HSN have an edge. And, somewhat surprisingly, the two shopping channels have a relatively low customer overlap, so the acquisition will broaden QVC’s market.

In July, just 15% of QVC customers also shopped at HSN. After the acquisition, HSN will continue to operate as a separate televised brand, but QVC should be able to leverage the strength of its former competitor to boost its own business. This alone, however, may not be enough to put QVC in serious competition with Amazon and Walmart.

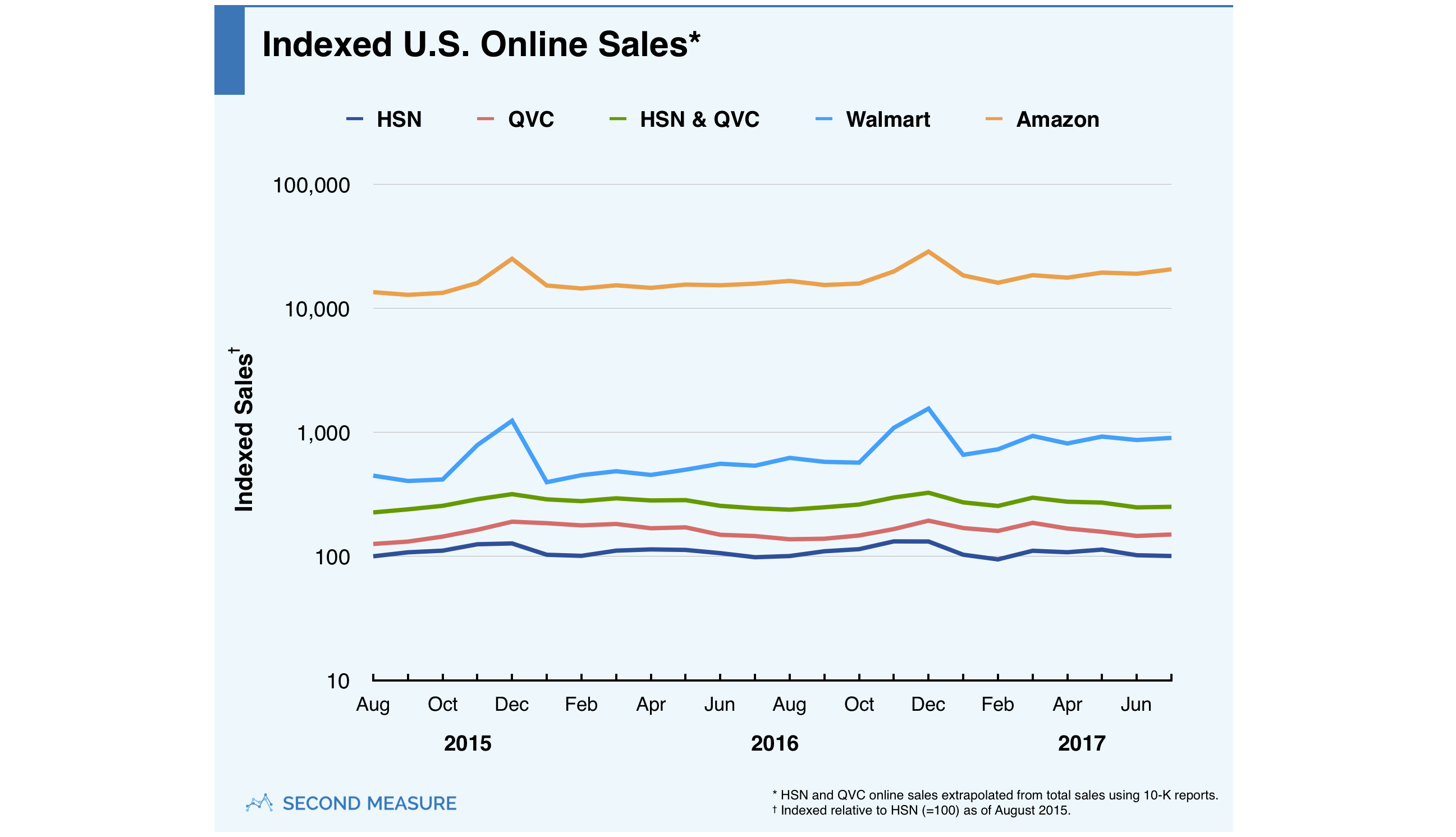

According to our data, Amazon and Walmart.com currently show higher online sales than QVC. The combined sales of HSN and QVC put the soon-to-be merged company closer behind Walmart’s web business, although both lag significantly below Amazon. Of course, it’s worth noting that the majority of Amazon’s total revenue comes from the sale of online products, while for Walmart, e-commerce only accounts for about 3% of total revenue. About half of QVC’s earnings come from online sales.

Many QVC Shoppers Don’t Shop at Amazon or Walmart

Amazon and Walmart have dominant lifetime market penetration: 73% and 77% of US consumers have ever shopped at each, respectively. For QVC, the key to staying in the race will be holding on to its existing customer base. Our monthly data shows that, in July, 55% of QVC customers shopped at Amazon, and 58% were Walmart customers. Furthermore, 22% of QVC’s July customers eschewed both Amazon and Walmart, giving hope that QVC can succeed by appealing to its distinct market.

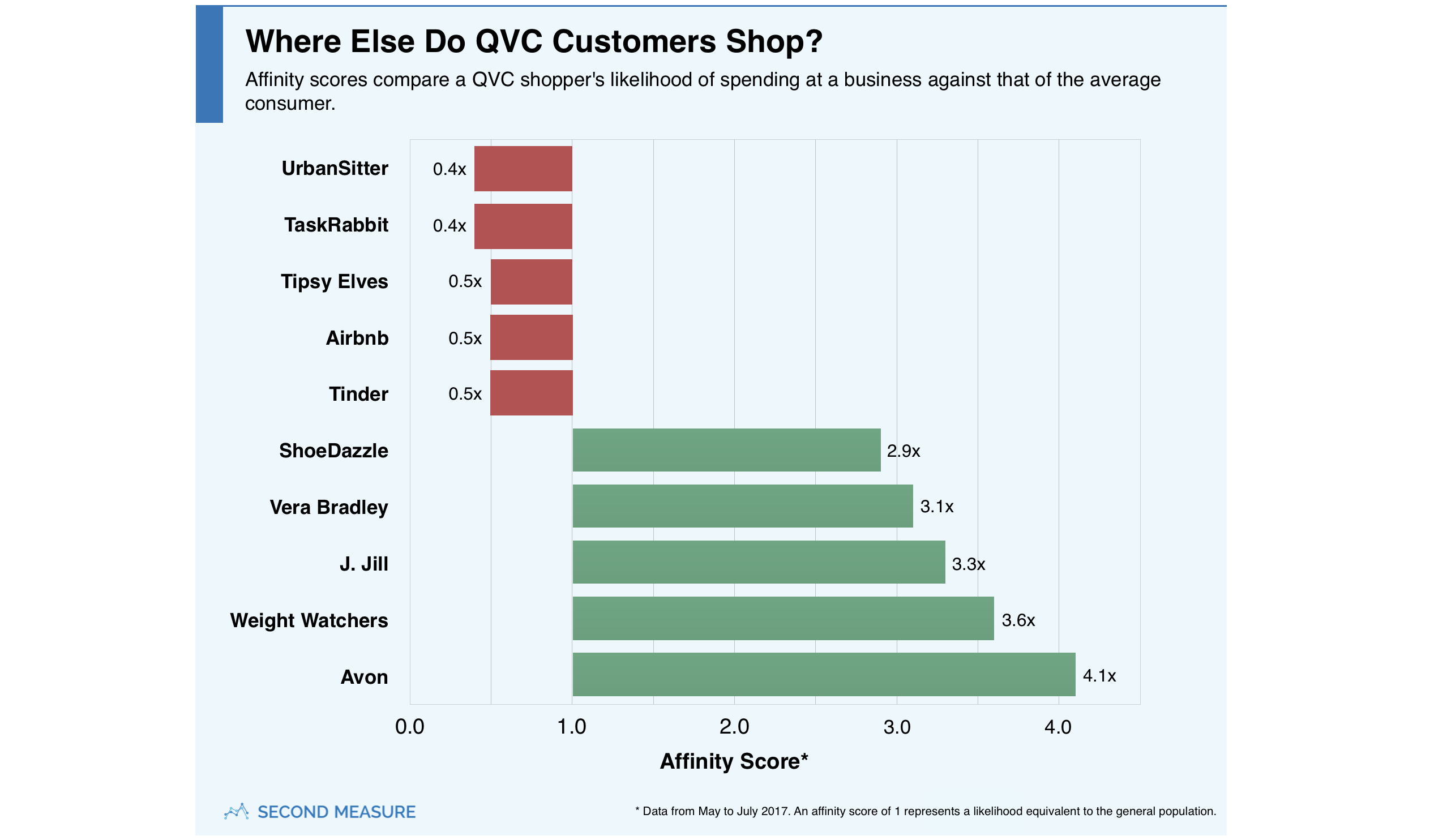

By analyzing billions of consumer transactions, Second Measure determines where else customers of a given company are most likely to spend, a metric we call customer affinity. Our data shows that QVC customers have positive customer affinity toward products marketed primarily to women. These TV shoppers are at least three times more likely than the general population to shop at J.Jill and Chico’s, which are both women-only retailers. QVC customers are similarly more likely to spend on several beauty brands, such as Avon, and accessory retailers like Vera Bradley, ShoeDazzle, and Gemvara. Equally popular are several diet programs, including Weight Watchers.

And although nearly half of QVC’s sales last year were made online, QVC customers show negative customer affinity toward several gig economy websites, which facilitate resource sharing and freelance labor. According to our data, a member of the general population is at least twice as likely as a QVC shopper to spend with companies such as Airbnb, TaskRabbit, and UrbanSitter.

Another clear trend among QVC’s customers is a negative affinity toward companies with a younger customer base. QVC customers are half as likely as the general population to spend on millennial brands such as Tinder, Reddit, and the online clothing retailer Tipsy Elves. It’s difficult to prove that QVC customers skew older, but the affinity trends we observe support this idea.

HSN Shoppers Spend More, but QVC Shoppers Buy More Often

Our data reveals other benefits the shopping networks likely considered in this sale. HSN’s shoppers spend more per transaction than QVC’s, making them an attractive acquisition for the brand. In July, HSN averaged $50 per transaction, beating QVC’s average of $33 and Amazon’s of $38.

Complementing HSN’s strengths, QVC excels at driving its customer base to make more frequent transactions. Our data shows its customers averaged 4.1 purchases in July, as compared to 3.2 for HSN.

Want to know whether the HSN acquisition will be enough to put QVC in serious competition with Amazon and Walmart going forward? Request a demo and continue following QVC customer and sales data.